Is it safe to accept a cashier's check when selling a car?

Blog Home

Updated on by Jason Hoetger

When selling a car, many sellers don't realize cashier's checks are extremely easy to forge and difficult to verify, making them one of the riskiest and least safe ways to get paid when selling your car.

Still, if you're selling a car private party, it is possible to safely accept a cashier's check if you take some precautions to make sure the check is genuine before signing over your title.

What is a cashier's check?

First, it's important to understand what potential buyers mean when they ask to pay with a cashier's check, certified check, money order, or personal check.

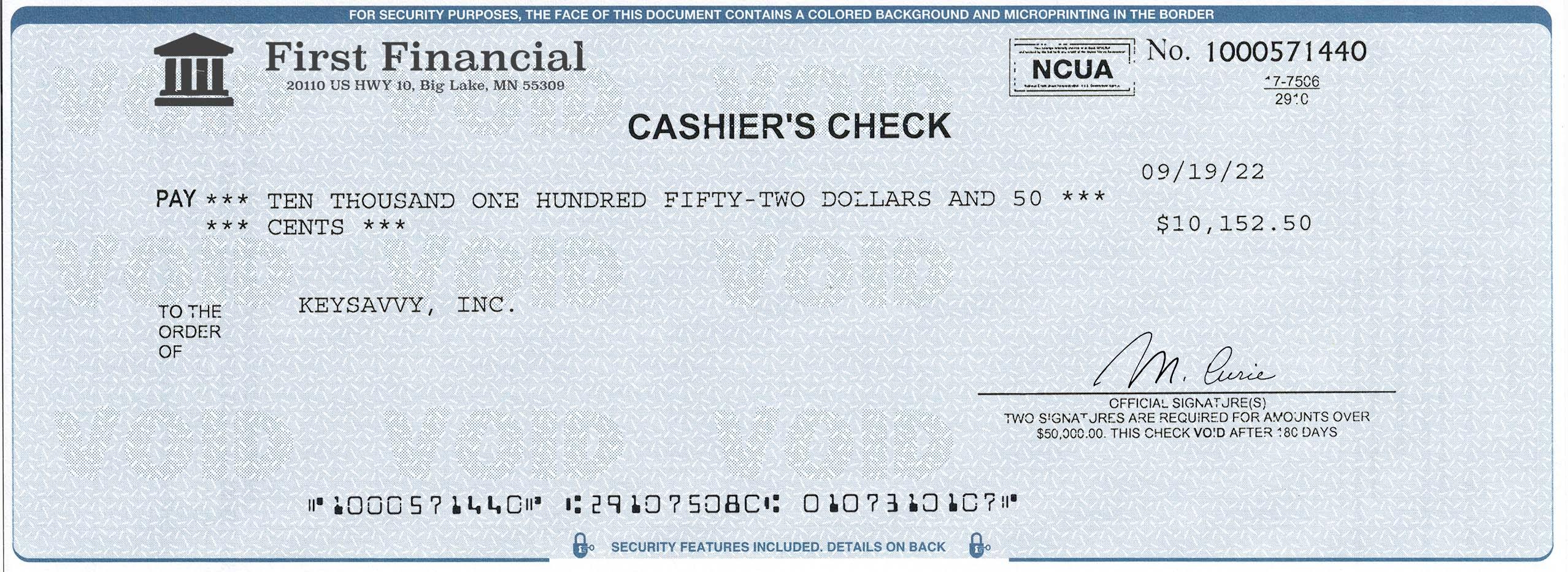

- Cashier's Check: A direct obligation on the bank itself, not on the buyer's account at the bank. When genuine, cashier's checks are FDIC insured and cannot "bounce" (be returned for insufficient funds).

- Certified Check: A certified check is actually a type of personal check that the bank guarantees will clear. The bank has verified the customer's signature and has already withdrawn the funds from the customer's account. Like a cashier's check, a genuine certified check cannot bounce.

- Money Order: Money orders are issued by companies that are not banks, but are similar in practice to cashier's checks. When a money order is genuine, it will not bounce.

- Personal Check: Unlike other types of checks, personal checks can bounce, even when they are genuine. If the person writing the check does not have enough money in their account, the check will not clear.

When you're selling a car, cashier's checks, certified checks, and money orders share the same benefits and risks: the funds are guaranteed, but only if the check is genuine. Personal checks are much riskier, however, because their funds are not guaranteed.

Why is accepting a cashier's check risky?

Cashier's checks are risky because it takes time for banks to process cashier's checks, so it looks like the check has cleared, even when it hasn't. The Office of the Comptroller of the Currency explains what happens when you deposit a fake cashier's check:

It can be very difficult for either you or your bank to tell [if the check is genuine]. When you deposit a check into your account, your bank generally is required by law to make the funds available within a specific period of time [...] This is true even if the check has not yet cleared through the banking system. Therefore, even if the funds have been made available in your account, you cannot be certain that the check has cleared or is "good."

Your bank may learn of the problem only when the check is returned unpaid by the other bank—which may take a couple weeks or more. Once the item has been returned unpaid, your bank will [...] collect the amount of the deposit from you.

By the time your bank discovers the cashier's check is fake, your buyer will be long gone--with the vehicle and a signed title in hand. Your only recourse will be in court, but if the buyer gave a fake name or address, it may simply be impossible to collect your funds or recover the vehicle.

How to safely accept a cashier's check

Despite the risks, it is possible to safely accept a cashier's check if you're willing to meet at the buyer's bank. Ask the bank teller to verify the check for you before you sign over the title. If the buyer refuses to meet at their bank, consider that a major red flag.

Conclusion

If your buyer has a local bank and you both are willing to meet there during banking hours, cashier's checks are a good option for private party car sales.

But if your buyer doesn't have a local bank, or you simply don't want to meet at their bank during banking hours to manually verify their check, consider more convenient alternatives such as KeySavvy to verify the buyer's funds and guarantee you get paid.

Buy and sell cars worry-free

KeySavvy makes it safer and easier to buy and sell cars on any marketplace.